Rules for Startups Raising Capital in the Midwest – Part 5: Investor Outreach

Rules for Startups Raising Capital in the Midwest – Part 5: Investor Outreach

Tom Walker

Note: “Rules for Startups Raising Capital in the Midwest” is a multi-part Entrepreneur Toolkit series based on Rev1 Ventures Capital Access Learning Lab. We suggest you review the preceding sections: Part 1 – Basic Information on Venture Capital, Part 2 – Capital Planning Worksheet, Part 3 – Building Your Investor List, and Part 4 – Due Diligence.

Funding raising is hard, especially in the Midwest. A smaller capital pool equals more competition. The best way to compete and succeed is to plan, prepare, and execute.

A key aspect of your plan is building relationships with potential investors at least a year before you expect to need funds. Strengthen those relationships as you achieve the milestones of your business plan with the intention of fundraising in earnest with at least six months of runway.

There will be a lot to accomplish in those six to twelve months. It takes at least six months (wise entrepreneurs plan for more) before active fundraising, to build your capital access plan, and prepare for due diligence.

Once you become an active investment prospect (when investors start requesting information), diligence closing (responding to those requests and the questions that follow) will likely take another six months. The process is one of lines, not dots. Demonstrate a progression of business progress that meets the milestones of your business plan.

Fundraising Is a Sales Process

Model your fundraising process on the best practices of customer acquisition.

Approach your plan with a sales funnel mindset. With qualified and prioritized investors set up in your CRM (customer relationship management) system, use email analytics to track touchpoints and open and click metrics. Examples of tools and resources are listed below.

- Ensure deal room and due diligence documents are ready to go and aggregated in a secure, online document collaboration platform, such as Box

- Compile investor list from Crunchbase

- Upload list into your customer relationship management system (CRM) or Foundersuite

- Upload deck into a secure mail solution, such as DocuSend or PandaDoc

- Draft template email in CRM

- Send contact email within your email management platform

- Track opens, clicks, and email analytics

- Schedule follow-ups based on replies.

- Annotate specific details from their response such as metrics, stage, or traction necessary for raising capital

Additional tools and resources

- Investor Databases and Places to Connect: FounderSuite, Signal, VC, Crunchbase

- Email Tracking: Mailchimp, Bannanatag, Boomerang

- CRM: Salesforce, HubSpot

- Documents Tracking: DocuSend for deck analytics

- Connection Research and Contacts: https://www.linkedin.com/ (export contacts, search connections)

Effective Email Communications

Be thoughtful when you compose your emails. Develop a personalized template that works for you. It is practical and efficient to standardize a structure and some aspects of your message.

Example: Investor Outreach Content

Each element of an effective investor email will answer these questions.

- Why should the investor open your email?

- Legitimize who you are and your connection with the investor? (Do you have any personal ties?)

- What problem is the startup solving and what’s the solution/product? Is it clearly understood?

- Does the startup have empirical evidence supporting the business model and momentum?

- Is this the right team for the job? Do they have direct experience/credible people?

- What is the startup asking from me, the investor?

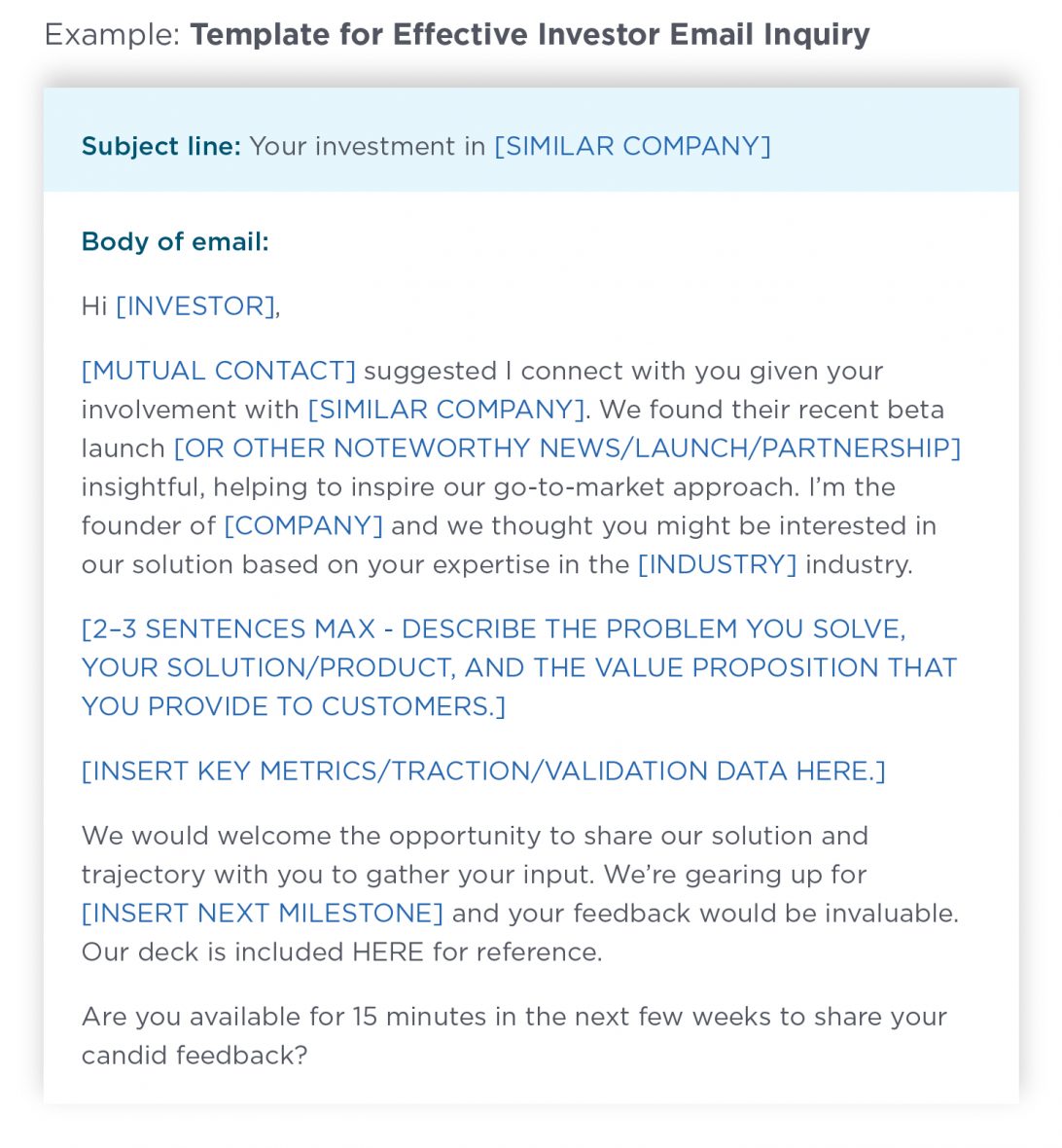

Example: Template for Effective Investor Email Inquiry

Example: Sample Investor Email Inquiry

![]()

Ideally, a mutual connection will introduce you to a potential investor. If so, mention that in your email. However, do not EVER claim to have a mutual relationship with a connection if it does not truly exists. It is surprising how many company founders try this trick. That violates the most essential aspect of an investor/startup relationship—trust.

Best Practices and Pitfalls for Email Outreach

Best Practices

- Achieve an introduction through mutual connections. Cold outreach is a last resort.

- Research the individual and their firm before reaching out.

- Personalize your message.

- Be brief. Limit your email to one to two sentences per section, with 2-3 sections total.

- Avoid business jargon and acronyms.

- Limit links and attachments in the first email to avoid ending up in a spam folder.

- Highlight your differentiators.

- Quantify your value proposition and milestones.

- Include a call-to-action . Example: “Are you available for a 15-minute call in the next week or two to provide candid feedback?”

- Build the relationship first before asking for money.

- Appeal to their altruistic nature; consider asking for advice or expertise on a specific matter based on their experience.

- Track emails (opens and clicks on links).

- Use a CRM to track the entire process and notifications/triggers for follow-up reminders.

- Proofread, and then proofread again to avoid misspellings and errors.

Pitfalls

-

- Don’t bombard. Don’t assume any investor will respond immediately. Give it a week before following up.

- Don’t use illogical language. Avoid statements like “This is a 50X ROI opportunity, guaranteed returns in 12 months, very conservative forecasts, best deal you’ll ever see, once in a lifetime opportunity, etc.”

- Keep your email simple. Don’t overly format with fonts and colors.

Investor Updates Are Powerful Tool for Fundraising

Regular investor updates are a high-leverage activity for CEOs. Ask potential investors if you can add them to your regular investor updates to track the business’s progress. Do this BEFORE you need to raise.

Provide high-level, non-confidential company news about teams and hiring, business development, product launch, referenceable customers (with their permission), and critical partnerships.

Hearing about your progress and needs informs existing investors so they know how and when they can help. Turning milestone dots into connected lines of progress may help move hesitant investors over the fence when you finally accomplish the appropriate milestones.

Interpreting Investor Replies

Fundraising is an iterative process. You can’t get to yes without a series of nos. Every question, pushback, or objection is a moment to collect and gather feedback. Don’t be afraid to dig deeper into why your company isn’t a fit for an investor.

When you don’t know the answer to a question, figure it out. If one person asked the question, the chances are that someone else will request it too. Consider all the feedback you receive. You don’t have to act on everything. Not all feedback is relevant. Plus, VCs won’t always say what they think.

An investor’s issues may be with the company, for example, lack of traction, lack of a coherent story, or a lack of direct experience or expertise. These are issues the company must try to fix. If one investor has these concerns, likely so will the next.

However, a VC may reject your deal for issues of their own. These could include lack of capital or dry powder for subsequent rounds, competitive investments or conflicts of interest, or even previous bad experience in the sector.

Listen, consider, then act. Over time, you will learn to discern which information you should add to your deck and which information you hold back. Many more VCs will pass on your deal than will invest. Reflection is critical, but don’t overthink their response. Your company cannot be everything to everyone.